For a long time, there was a stigma around using traditionally for-profit terms like “marketing”, “sales” and even “income” for non-profit organizations, especially those who are faith-based. But the reality is the best run organizations function much like businesses, in both their front and back office operations. And in much the same way publicly traded companies are accountable to their shareholders, it is incumbent upon charitable organizations to manage their donors’ contributions responsibly. With that in mind, I won’t waste your time discussing business practices you already know, but instead we can focus on the differences in the non-profit sector.

For a long time, there was a stigma around using traditionally for-profit terms like “marketing”, “sales” and even “income” for non-profit organizations, especially those who are faith-based. But the reality is the best run organizations function much like businesses, in both their front and back office operations. And in much the same way publicly traded companies are accountable to their shareholders, it is incumbent upon charitable organizations to manage their donors’ contributions responsibly. With that in mind, I won’t waste your time discussing business practices you already know, but instead we can focus on the differences in the non-profit sector.

The easiest way to evaluate a non-profit’s finances is to look over their Form 990. This is the IRS 501(c)3 version of a federal tax return. Organizations with a religious designation are technically not required to file a 990, but filing one illustrates financial transparency and gives you the information necessary to evaluate them. So even if it is not required, the lack of a Form 990 could be a red flag. There are numerous websites out there which allow you to quickly and freely access an organization’s Form 990, but 2 of the most popular are Guide Star and Charity Navigator.

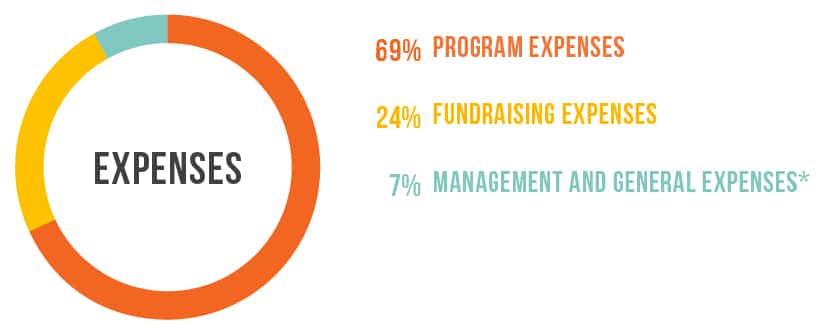

When looking over 990, you’ll see 3 primary classifications that the IRS uses for categorizing expenses: Program Services, Admin and General, and Fundraising. The general rule of thumb is that the vast majority of expenses should be going toward Program expenses. There is some variation in the exact ideal percentages, based on the specific type of work an organization does, but a rough guideline is: 75% Program Services, 15% Admin and General and 10% Fundraising. I’ve taken up more time than I wanted, but I want to spend a brief moment to point out why above average admin and fundraising expenses should be a concern.

If you see a questionably large amount of money allocated toward admin, then look more closely at the 990 to find the executive compensation. This is the most likely culprit and could indicate a lack of commitment to the organization’s mission.

If you see a questionably large amount of money allocated toward admin, then look more closely at the 990 to find the executive compensation. This is the most likely culprit and could indicate a lack of commitment to the organization’s mission.

As for fundraising, I’ve read articles recently saying that 10% is no longer a realistic threshold. The justification is that the new wave of online fundraising services and tools available could push an organization’s expenses in this area higher. While I agree that there are good tools that cost money to use, they are often offset by reduced travel costs. And many of these tools are geared more toward building awareness, which they IRS allows to be classified as Program Service. I believe that an above average fundraising budget indicates inefficient fundraising events, such as disproportionately extravagant galas.

Next Topic: Sustainability